| X |

Butterfly brooches in LA show |

X |

| |

Sixteen spectacular brooches—elegantly

designed in butterfly motifs and fashioned from 18K

gold and rare gemstones—are now on the display

at the Natural History Museum of Los Angeles

County.

The pair who are the owners and creators of

the Butterfly Brooch Collection prefer to remain

anonymous, but it’s hard to fully appreciate this

remarkable collection without knowing

something about them. Business partners for several

decades, they combine a perfect mix of abilities: a

passion for rare gems and a desire to share their

passion with the world. That is what drove them to

create their remarkable butterflies—as well as a

much more extensive collection of jewellery set with

rare gems that they’ve been assembling since the

mid-1970s.

One is a master gem cutter who is recognized

worldwide for his skill in cutting the rarest of gems.

He also knows his way around a “hole in the

ground” and actually mined many of the gems he

has cut. The other is a wonderfully gifted jewellery

designer who knows, perhaps better than anyone,

how to take best advantage of the unique beauty inherent in such exceedingly rare gems.

Each of the butterfly brooches has its own

fascinating story. Among the rarest and most

noteworthy of the stones seen in the butterflies is

benitoite, California’s state gem. One of its

owners began working the Benitoite Gem mine

(also known as the Dallas mine) in San Benito

County, California in 1967, and continued for

33 years. He is responsive for both mining and

cutting much of the world’s supply of this rare gem,

because this mine is the world’s only source of gemquality

benitoite. Now, the mine is considered

exhausted. This butterfly has a total of 34.67 carats

of benitoite.

Two butterflies in the collection feature vivid

orange spessartine garnets from the Hercules Dike at

the Little Three mine in Ramona, California. This is

another deposit that one of the owners worked

for many years. The mine is now surrounded by a

housing development.

|

The beautiful shocking pink centre stone gives

this brooch its name—the Rhodochrosite butterfly

Brooch. In addition to rhodochrosite, this brooch

features apatite, opal and titanite gems—all from

Mexico.

The Pearl Butterfly Brooch features natural

pearls from the Sea of Cortez (also known as Baja

pearls). The Spanish explorers in the early 1530’s

noticed that the Pericu Indians had necklaces

made of these pearls. The recovery of pearls

became a priority for the Spanish as

they established settlements on the Baja Peninsula,

and the Baja pearl industry grew to supply many of

July 2012 Bangkok Gems & Jewellery 39

the world’s pearls in the 19th century. Softly

coloured rainbow feldspars from Madagascar were

also included in this brooch to set off the pearls,

and the vivid green eyes are Colombian emeralds. |

|

|

| |

|

|

|

|

| |

Couture Design Awards 2012 |

|

| |

| |

|

|

Couture, with its rich history of hosting the

world’s most coveted designer brands, recognized

the pinnacle in fine jewellery design for 2012 at its

Couture Design Awards. The annual programme,

held last month at the Wynn Las Vegas, recognized

winning designers in 10 categories as well as the

recipients of the People’s Choice Award and the

Couture Time Awards.

Judging the entries were Susan Abeles,

director of jewellery for Bonhams; Eric Ford, precious

jewellery buyer at Neiman Marcus; Janice

Blumberg, owner of Be on Park; Alison Rowe,

fashion and accessories editor for Niche Media;

Claudia Mata, jewellery and accessories director for

W Magazine; and jewellery designer Stephen

Webster.

|

xx |

|

Couture Time Awards

Romain Jerome’s Steampunk Chrono, a 50-

milimetre retro-futuristic

timepiece with 42-hour

power reserve, won in the

Couture Time Awards’

Architecture category.

HD3 Slyde’s domed

sapphire touch screen

timepiece, presenting a

bevy of virtual functions

and complications, took the Couture Timepiece Award for Innovation. |

|

|

| |

|

|

Up to down

Bridal

John Apel was the winner

in the Bridal category with

this platinum engagement

ring with pear-shape,

marquise and round rosecut

diamonds.

Silver

This bangle, made with

38 carats of rainbow

moonstone and white

topaz and set in black and

white rhodium-plated

matte silver, is from the

Lauren Harper Collection

and won in the Silver

category. |

|

|

Human Spirit Award

The Couture Design Awards also recognized

Jim DeMattei, president of ViewPoint, with the

Human Spirit Award, which honours a member of

the Couture community who stands out for

exceptional generosity of mind and spirit. |

|

|

Diamonds Above

$20K

Stephen Webster won

in the Diamonds

Above $20K category

for his Temptation of

Eve ring, which

features 7.75 carats

of Forevermark

diamonds, 3.34

carats of white pave

diamonds and black

onyx set in 18-karat

white gold. |

Gold

Majoral’s 18-

karat yellow

gold necklace

won in the

Gold

category. |

x |

|

|

|

Pearls

Mikimoto’s baroque black

South Sea cultured pearl and

diamond ring, set in 18-karat

white gold, took first place in

the Pearls category. |

Coloured Gemstone Below

$20K

Rodney Rayner won in the

Coloured Gemstone Below

$20K category with his Via

Roma ring, made in 18-

karat rose gold with orange

sapphires, champagne

diamonds, white diamonds

and irregular faceted

citrine and smoky quartz

centres, with a citrine centre

stone. |

|

|

|

|

The Couture Design Awards recognize the best in fine jewellery design. |

| |

Graham London’s Silverstone Tourbillograph,

an automatic one-minute tourbillon chronograph

wristwatch, won in the Technical category of the

Couture Time Awards.

Bremont’s aviation-inspired ALT1-WT watch

took first place in the inaugural People’s Choice

category of the Couture Time Awards. |

| |

|

|

Platinum

Heinrich &

Denzel’s Arcus

bangle with 268

brilliant diamonds

set in platinum

took first place in

the Platinum

category. |

Diamonds Below

$20K

This bracelet by

Moritz Glik with

rose-cut and

brilliant-cut

diamonds

enclosed in

double white

sapphires in 18-

karat yellow gold

and blackened

silver took first

place in the

Diamonds Below

$20K category. |

|

|

|

| From left: Jan Mohr, of Couture retailer relations; Jim DeMattei,

president of Viewpoint; David Rocha, executive director at Jewelers

for Children; and Chris Casey, publisher of National Jeweler and vice

president of Nielsen’s jewelry exposition group. |

Coloured Gemstone

Above $20K

This bangle by Lydia

Corteille is made in

18-karat gold with

brown diamonds,

tsavorites, green

turquoises and

emeralds and took first

in the Coloured

Gemstone Above $20K

category. |

|

|

|

|

Debuting at Couture

Sevan Bicakci was

recognized with the

Debuting at Couture

Award for his Magical

Peacock pendant, made

with silver, white and

brown diamonds and a

carved rutilated quartz

centre stone set in 24-

karat gold.

|

People’s Choice

The People’s Choice

Award was given to Kwiat

for these platinum and

diamond earrings from

the Legacy Collection. |

|

|

| |

|

|

|

|

| |

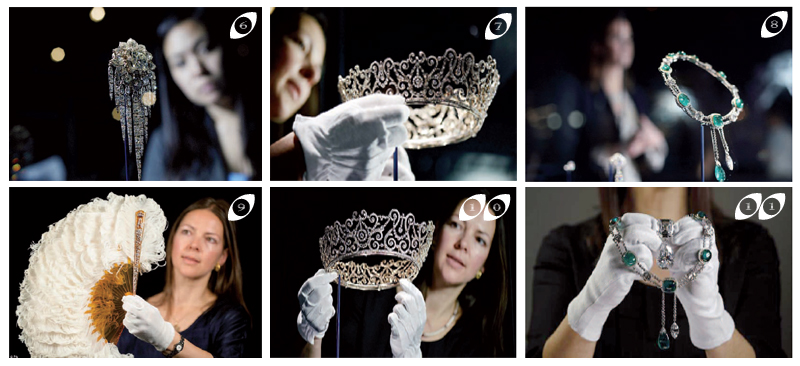

Queen Elizabeth's 10,000 diamonds on display in London |

|

| |

|

|

| |

1 & 2 The Jaipur Sword and

Scabbard, set with 719

diamonds weighing a

total of 2,000 carats,

originally presented to

King Edward VII for

his coronation in 1902.

3. The Coronation Necklace.

4. The Diamond Diadem Tiara, worn by Queen Elizabeth II on British

and Commonwealth stamps, also features on some issues of coinage

and bank notes.

5. Exhibition curator Caroline de Guitaut holds the Cullinan Brooch. |

|

| |

More than 10,000 diamonds go on show at

London’s Buckingham Palace this month to mark

Queen Elizabeth’s 60th year on the throne. The

exhibition, which runs from July 31 to October 7, was

designed to coincide with the queen’s diamond jubilee

this year, and features jewels Her Majesty wears regularly

at official functions in Britain and abroad.

The aim of the exhibition is to show how rulers

have used diamonds as visible signs of wealth and

power,” said curator Caroline de Guitaut, who described

the crowns, tiaras, rings, earrings, swords and snuff box

on display as “priceless.” De Guitaut said the 86-yearold

monarch was consulted on what would be used for

the exhibition, housed in a darkened room inside

Buckingham Palace and accessed via gilded,

colonnaded corridors lined with royal portraits going back generations.

“We have

tried to showcase

some of the very

most important

diamonds in royalpossession.” The

first item on show

in a brightly lit glass

case is Queen

Victoria’s small

diamond crown

which, despite its

size, features more than 1,100 diamonds. After her

husband Prince Albert’s death in 1861, Queen Victoria,

the only other British monarch to have marked a

diamond jubilee, wore only mourning clothes, meaning

that colourless stones such as clear diamonds were an

ideal adornment. Queen Victoria was regularly pictured

wearing it, including in her official diamond jubilee

portrait.

|

|

| |

|

|

| |

6. Queen Victoria’s Fringe Brooch. 7 & 10 Caroline de Guitaut, Curator of Royal Collections, holds the Delhi

Durbar Tiara, which was loaned to the Duchess of Cornwall in 2005.

8. A view of the Cullinan VII (Delhi Durbar Durbar Necklace and

Cullinan Pendant) 9. A diamond-set Coronation Fan, made for Queen Alexandra at the

time of the coronation in 1902.11. Exhibition curator Caroline de Guitaut poses with the Cullinan VII

necklace. |

|

| |

Perhaps the most impressive display, however, is

that containing seven of the nine major stones cut from

the Cullinan Diamond, the largest ever found. The

stone was discovered in South Africa in 1905 and was so large that a clerk working at the mine initially threw

it away, assuming it was a worthless crystal. Eventually,

though, the stone weighing 3,106 carats in its rough

state, was presented to King Edward VII who decided

to have it cut and polished. It produced 9 principal

stones and 96 small brilliant diamonds. The two main

gems, the largest colourless and flawless cut diamonds

in the world, were set in the Sovereign’s Sceptre and

Imperial State Crown.

Like many of the important diamonds in the

exhibition, Cullinan III and IV were used in a variety of

settings over time, but today form a brooch worn by

Queen Elizabeth at a service of thanksgiving at St.

Paul’s Cathedral last month. Cullinan V is in a brooch,

Cullinan VII hangs as a pendant from an emerald

necklace, Cullinan VI and VIII are also in a brooch, and

Cullinan IX, the smallest of the nine main stones at 4.4

carats, is set into a platinum ring.

Underlining how diamonds were used as gifts of

diplomacy as well as objects of desire, Queen Victoria’sfine fringe brooch

includes the stones

presented to her by

the Sultan of Turkey

as a token of thanks

for Britain’s support

in the Crimean War.

Victoria appears not

to have appreciated

the sultan’s tastes,

and had the jewels

reset.

|

|

| |

|

|

| |

12.Diamond encrusted: A table snuff box owned by Frederick the Great

of Prussia, incorporating nearly 3,000 diamonds, which was

purchased by Queen Mary in 1932.

13. A vitrine containing Queen Mary’s Girls of Great Britain and Ireland

Tiara.

14. The Queen’s Williamson Diamond Brooch.

15.The Diamond Diadem. |

|

| |

The Jaipur

Sword and Scabbard

were presented to

King Edward VII for

his coronation in

1902 by the Maharajah of Jaipur, and have been set

with 719 diamonds weighing 2,000 carats in total.

More recently, Queen Elizabeth was gifted the

Williamson Diamond in 1947 by Canadian geologist

and royalist John Thorburn Williamson, and it is

considered the finest pink diamond ever discovered. From its original uncut 54.5 carats it was cut into a 23.6-

carat round brilliant stone and now sits in the centre of

a flower-shaped brooch by Cartier. While de Guitaut

said she could not even guess the value of the diamonds

on display, a pink diamond of similar size without royal

provenance, fetched $46 million at an auction in

Switzerland in 2010.

Of all the royals represented in the exhibition,

Queen Mary’s name came up most often. Queen

Elizabeth’s grandmother clearly had a passion for

jewellery, and among her acquisitions was a snuff box

made originally for Frederick II of Prussia and his court.

The box is covered with nearly 3,000 diamonds,

including many on the bottom which would normally

be invisible, and came to England after the Russian

Revolution. There it was sold twice before being

purchased by Queen Mary in 1932. |

|

| |

|

|

| |

Recycled Diamonds Integral to supply |

|

| |

“Last year was an excellent

year for us,” said the outgoing De

Beers chairman Nicky

Oppenheimer at a party with clients. “If you didn’t make money, then

you are obviously in the wrong

business,” he semi-quipped before

a stunned audience. Looking at the

macroeconomics of the diamond

pipeline from rough production to

wholesale sales of polished, the

trading and manufacturing sectors

as a whole did not make money on

their trading activity, though they

earned on inventory appreciation.

Those who restocked rough

in the first eight months of 2011

saw DTC rough selling prices rise

by some 44 percent, just to witness

a steep fall of some 16 percent in the

last part of the year. The DTC clearly

abandoned its time-honoured policy

of only raising prices to so-called“sustainable” levels. Looking at the

composite price index, for all

qualities and sizes, we saw a

doubling of rough prices in the past

two years again outpacing the

increases in polished, only to end at

lower levels.

A Good Year?

If we take an average 15-20

percent in inventory appreciation

over the year (including polished),

the industry did make US$2-US$3

billion overall, though this would

be because of higher prices – and

through no efforts by the players

themselves. The euphoria expressed

by Nicky Oppenheimer was, in a

sense, not “out of place”; but it was

a “good year” for the wrong

reasons. Also, a large part of the

(potential) paper earnings remain

in inventory until they materialize,

thus, actually, representing “future

music.” So, last year was excellent

if you were a rough producer or a

jewellery retailer. That is where the

real profits were, and, of course,

these are the core businesses that

the Oppenheimer family has now

sold to Anglo American.

|

|

| a) Mr Claim Even-Zohar b) Mr Nicky Oppenheimer |

Looking at the Pipeline

As it takes about a year and a

half for a diamond to move through

the value chain from rough

acquisition to polished sales (at

polished wholesale prices), the price

volatility has made it far more

challenging to present an accurate

picture for the year that was. Even

producer countries vary in their

reporting methodologies of mining

output values.

Just look at the volatility in

the reported average values of world

(run of mine) output, which totalled

about US$95 per carat in 2008,

plunging to US$72 per carat in

2009, recovering to US$98 per carat

in 2010, and then climbing to

US$121 per carat in 2011. This

shows an enormous (and

unsustainable) jump. For 2012, we

expect the average world output to

decline to US$108 per carat, also

because of the expected stepped-up

production from the (cheap goods)

Argyle mine and growing Marange

output.

Last year, natural diamond

production came to some 125-130 million carats valued at US$15.2

billion. This output moved through

the pipeline resulting in US$22.6

billion worth of polished. The

overhang in the 2011 pipeline is an

estimated US$1.3 billion of rough

and polished expressed in polished

wholesale prices at year end. It is

this overhang that will also impact

the rough demand for 2012.

Worldwide diamond jewellery

retail sales came to

US$70.8 billion. The market share

of America in diamond consumption

was reduced to 38 percent. The

other major traditional market,

Japan, declined further to merely

an 8 percent share. In a neck-toneck

race to be the second-largest

diamond-consuming nation is India,

with 12 percent market share,

followed by China (the mainland)

with 11 percent. Hong Kong is

accounting for 2 percent. |

|

| c) Argyle mine d) A model displays diamonds at a De Beers Show. Recycled diamonds, experts say, could be devaluing the minerals used in engagement rings and necklaces. |

The Recycling Factor

The value of the diamond

content in retail sales in 2011 came

to US$23.6 billion. The vast majority

of this amount (US$22.6 billion)

comes, of course, from either

recently mined rough or inventories.

The new reality is, however, that

some of the polished comes from

recycled diamonds — diamonds that

consumers have held for many years

or even for generations but now felt

the need to sell in order to pay

mortgages, medical care, children’s

education or even to supplement

pensions or to pay debts.

We want to be very careful

here — this is definitely not a new

phenomenon. Anyone who has

followed the trade of pawn shops or

is familiar with high-street family owned

jewellery businesses knows

that there has always been an

element of selling off “old” estate

jewellery. Many New York diamond

manufacturers have built quite a

reputation for their “re-cutting

skills,” turning old shapes into more

fashionable goods. However, since

the advent of the last economic

crisis, the volumes of diamonds held

by consumers coming back into the

pipeline have skyrocketed. Literally

hundreds of diamond businesses

have developed special niche

expertise in this area. Those recycled

diamonds are mostly sent to India

or other cutting centres for recutting.

A large part of the diamondrecycling

supply side takes place in

invisible parallel markets, defying

effective monitoring. It’s easier to

measure gold recycling, as there,

the jewellery needs to be refined

through a limited number of known

refineries. When, in early 2009,

jewellery scrap fabrication

exceeded new mining supplies, one

got a further indication of the

intensity of this movement of goods

back into the pipeline.

We have estimated that

recycled diamonds sold again to

the jewellery sector came to about

US$1 billion in 2011, which

represents 4.4 percent of all polished

diamonds sold at polished wholesale

prices. This is quite significant, and

it has definitely become a supply

factor that requires serious thought

by pipeline participants, especially

producers, when estimating supplyand-

demand trends. They do tend

to soften polished retail prices, as

retailers’ huge profits on recycled

goods allow them more breathing space in selling polished. |

|

| e) The 2011 diamond pipeline

‘Global Household Mine’

Just as one is very conscious

about the depleting diamond

reserves of existing mines, it is

worthwhile to take a look at what

the so-called “Global Household

Mine” has in stock. What are its

potential reserves? Unfortunately,

diamonds last forever… they don’t

just disappear, nor are they being

thrown away together with old

furniture, books or other junk piling

up in people’s attics. The supply of

recycled diamonds is driven by

various functions — not only by

economic necessities but also by

the high prices.

One tends to assume, or one

likes to believe, that diamond

possession is solely a very

emotional phenomenon, but this is

not universally true. In India, for

example, diamonds and gold in the

hands of consumers are often viewed

as assets. In parts of the Arab world,

this holds true as well. So what are the Global Household Mine

reserves?

Since ancient days, diamond

mines have produced some 5.2

billion carats, which at 2011 rough

production values (US$121 per

carat), would amount to some

US$625 billion worth of rough. The

historically adjusted gem-quality

polished output would be between

1.3-1.6 billion carats. (Traditionally,

no more than 15-20 percent of

output was considered cuttable; that

changed in the 1960s with the

emergence of the near-gems.) The

worldwide average polished sale

price (at polished wholesale prices)

is US$625 per carat. Therefore, the

Global Household Mine probably

holds US$0.7-US$1 trillion worth

of polished diamonds at current

prices. About 40-50 percent of these

diamonds would be held in America.

This is a staggering amount.

In 2011, about a minimum of

US$1 billion of recycled polished

came back into the market — which,

by value, represents 4.4 percent of

polished retail demand. (It could be

more but it won’t be less.) The

really amazing, if not frightening,

figure is the “stock withdrawal” of

the Global Household Mine: the

US$1 billion figure represents

merely 0.1 percent of stocks by

value. Indeed, theoretically, the

Global Household Mine could meet

the consumers’ requirements, at

current levels, for about 35-45

years! As most women will not likely

depart from their diamonds that

easily, it is certainly not an

immediate concern. But it must be

part of a proper pipeline analysis.

There is an additional “recycling”

market in the making: investment

diamonds. So far, a dozen or so new

companies or structures purchase

polished for investment purposes.

These diamonds will come back in

at some point, but now there are

mostly buyers and not sellers.

|

|

Retail Environment

Everything is relative. Though

mining costs in absolute terms may not have increased so much since

2008, the higher price levels of the

output have dramatically doubled,

and in some instances, even tripled

mining profits. This is quite evident

in the evolution of profit sharing in

the value chain.

There are other pipeline

parameters that have gradually

changed over time, making them

less valid for comparison. The total

retail value of diamond jewellery

pieces is one of these. An analysis

of the diamond content in the final

jewellery product shows that the

ratio between diamond and other

used materials/costs has changed.

A decade or so ago, diamond

content (at wholesale polished

prices) would represent about 20

percent of the jewellery piece’s total

retail price. In some countries, like

England for example, it was even

less, more like 18 percent.

On the other extreme, there

were markets (such as Indonesia)

where diamond content might have

been at an average 60 percent of the

total diamond jewellery piece. This

has to do with overheads, retail

structure, taxes, etc. So, worldwide,

diamond content might have been

at averages of some 21 to 22 percent.

This has gradually changed.

Our research indicates that,

worldwide, the share of diamond

content in jewellery pieces has

increased to some 32 percent. There

are many reasons for this. One factor

is the shift of markets from the

United States (the so-called “junk

market”) to the far more valueconscious Far Eastern market. The

higher gold price has also

contributed to containing more

diamonds and less gold in an

industry that is at pains to meet

certain price points. Also less

expensive materials are increasingly

being used in the final product.

So, our global diamond retail

sales figure of US$70.8 billion

actually holds more diamonds (by

value) than this figure would have

contained a decade ago. (Or, to say

it differently, taking the US$23.6

billion of diamond content sold in

2011 (which we consider a hard

figure), and if one would

hypothetically assume only 22

percent wholesale diamond content

in the final retail piece, worldwide

diamond retail consumption would

have been calculated at US$100

billion.) |

|

But this clearly isn’t the case;

it is merely pointed out, as some

analysts may also arrive at higher

diamond jewellery retail values for

a variety of reasons. This often has

more to do with methodology and

data collection than with anything

else. Tacy Ltd. has done its pipeline

for 23 consecutive years, and we

believe our figures closely represent

the reality. We recognize, however,

that some researchers base figures

on telephone surveys of consumers,

on feedback from jewellers, on

financial reports from large retailers,

or statistics, etc. For the diamond

industry, there is only one figure

that really counts: how many

diamonds were sold in 2011. That

figure is US$23.6 billion at polished

wholesale prices.

2011 in Perspective

In the pipeline, each and every

diamond is only counted once, and every stone is basically cut and

polished only in one principal

location. Looking by value, we see

now that close to 70 percent of all

diamonds by value are

manufactured in China and India,

with some 13 percent in the southern

African and Russian beneficiation

countries. The role of Belgium,

Israel and the United States as

traditional cutting centres has

gradually been diminished to close

to insignificant figures. In terms of

manpower, these latter countries’

cutting labour force can be

measured in the hundreds rather

than in the thousands. In terms of

“number of stones,” we certainly

can say that 14 out of 15 diamonds

are cut and polished in India and

China.

It is important to neutralize

“double accounting,” which is

difficult as every stone may move

many times through multiple

jurisdictions. If one looks at

Belgium, for example, its 2011

polished exports are close to US$15

billion, well over 30 percent higher

than the previous year. But in terms

of added value produced through

manufacturing, there wasn’t more

than US$200 million, and only

US$1.1 billion (7.5 percent of total

polished export value) can be

attributed to domestic

manufacturing. Like the Israelis and

Americans, Belgians do most of

their manufacturing in China,

southern Africa, Asia and elsewhere.

The 2011 pipeline likes to capture

the added value generated between

the various phases of activity.

The traditional conventional

wisdom that trading centres also

require domestic manufacturing has

valid marketing purposes as it adds

to the illusion that one can find

“freshly cut and polished diamonds”

in that market. That “wisdom”

definitely belongs in the past.

|

|

| |

|

After the Crisis

In terms of numbers, global

retail demand in 2011 increased by

10.3 percent compared to the

previous year. However, it is still

slightly below the 2007 pre-crisis

level. In 2012, our models,

developed jointly with my

colleague Pranay Narvekar of

Mumbai-based Pharos Beam

Consulting, show that global retail

demand is set to increase by 8.3

percent. This definitely takes us well

above the pre-crisis levels. The total

polished wholesale demand in 2011

of US$23.6 billion is about 19.4

percent above the previous year.

That sounds like a lot, but given the

price movements it doesn’t point to

an increase in volume terms. One of

the reasons for the year to have

been challenging is that in 2010,

polished demand from the cutting

centres was 38 percent above the

previous year. So, the growth

sentiment in 2011 was only half of

that experienced in 2010. This is not the time to discuss the ripple

effect, which clearly validates those

figures.

On the rough demand side,

2011 saw a 35.2 percent increase

over the previous year. This trend

will not continue, and our models

suggest that rough demand will

actually decline slightly in 2012.

The same counts for the cutting

centres. Though in 2011 we saw a

growth of polished demand of 19.4

percent, this will slow down to 6.2

percent in 2012. So, while 2011

was quite a trying year for the

downstream industry in which

profits mostly came from higher

diamond values, 2012, if anything,

will be more difficult.

There is also concern about

the producers’ pricing of rough.

There is strengthened fixation on

their bottom lines, which triggers

considerable rough price volatility.

As mentioned earlier, the historical

commitment to sustainable rough

prices is something of the past. BHP

Billiton pioneered the linkage of its

long-term contract prices to the

behaviour of spot-market auctions.

It seems that De Beers is following

in their footsteps and that the prices

secured by the Diamdel auctions

may well guide the pricing of DTC

sight boxes under the new threeyear

contract. Expect in 2012

continued volatility of 5-10 percent

in both directions — with the overall

price levels going sideways.

The cutting and trading centres

may be in for quite a squeeze in

2012. Earnings need to come from

activity rather than from stock value

appreciation. Actually, such a

squeeze shouldn’t bother the

downstream players too much —

they have grown used to it.

— Courtesy of Diamond Intelligence Briefs

|

|

|

| |

|

|

|