| |

IGJ Thailand - Bangkok's Mid-Year Fair Gets Positive Response from Industry |

|

| |

|

The initial announcement of the International Gems & Jewellery Thailand Fair 2013 has drawn much favourable response from prospective exhibitors, both in Thailand and abroad. |

|

|

|

|

|

Thailand’s only mid-year

gems and jewellery trade event,

the International Gems & Jewelry

Thailand Fair 2013 (IGJ Thailand)

will be held between 13-16 June

2013 at the Royal Paragon Hall

Exhibition & Convention Center

in Bangkok.

Located in the heart of

downtown Bangkok, within the upmarket

Siam Paragon megashopping

mall, the Royal Paragon

Hall brings a new dimension to gem

and jewellery trade shows in

Bangkok |

|

The city-central location

means the venue is easily accessible

by car, cab or sky-train.

And being situated in

Bangkok’s most exclusive and highend

mega-shopping mall, the IGJ

Thailand Fair can be accessed by

discerning retail shoppers – those

shoppers who appreciate quality

jewellery, and who are accustomed

to selecting and purchasing fine

jewellery and gemstones.

IGJ Thailand 2013 will offer

exhibitors the complete range of

exhibit categories, in jewellery, gemstones, equipment and services. |

|

The International Gems &

Jewelry Thailand 2013 Fair is being

marketed by BG&J Group,

publishers of Bangkok Gems &

Jewellery Magazine. BG&J brings

to this event considerable

experience in this particular field.

BG&J was instrumental in

establishing the tradition of an

annual Bangkok mid-year gem and

jewellery event, which was widely

acclaimed by the Thai gem and

jewellery industry. The International Gems &

Jewelry Thailand 2013 Fair is being

marketed by BG&J Group,

publishers of Bangkok Gems &

Jewellery Magazine. BG&J brings

to this event considerable

experience in this particular field.

BG&J was instrumental in

establishing the tradition of an

annual Bangkok mid-year gem and

jewellery event, which was widely

acclaimed by the Thai gem and

jewellery industry.

IGJ Thailand 2013 is being

organized and managed by Inter

Expo Management Co Ltd, a joint

venture of Tong Hua

Communication PCL and BG&J Co

Ltd. |

|

|

| |

|

|

| |

Speculation Threatens Diamond Industry

By Moti Ganz |

|

| x |

As president of the

International Diamond

Manufacturers Association, I

would like to express the pain

and shout out in the name of

all the diamond manufacturers

the world over. This is one in

a series of articles and

speeches in which I have tried

to persuade the rough

producers that today’s profit

is tomorrow’s loss.

Speculation has died — I shout in their ears. Soon there

won’t be any more manufacturers with factories and

obligations to employees and commitments to rough

suppliers. And then what will you do with the rough?

Until now all my calls have been like a voice in the

wilderness. Everyone understood exactly what I was

talking about but it was more comfortable for them to

put their hands over their eyes, ears and mouth —

knowing nothing, seeing nothing, hearing nothing —

especially as the cash register kept ringing. So that no

one gets tired before we get to the main point, I’ll begin

with the bottom line of what I have to say :

Once removed from the consumer’s mind,

diamonds will not get back there. Pearls and gem stones

will not wait patiently. They are beautiful, attractive and

valuable. Before you can say “Jack Robinson,” they

will take over the display windows. And if consumers

nevertheless want diamonds, they will quickly realize

(they are already starting to realize) that synthetic

diamonds are no less beautiful than natural ones, and

perhaps even more so. They will be able to get them at

comfortable prices, easily match pairs and sets and we

— the manufacturers — can finally gain something!

And then what will happen to rough diamonds? Will

they remain in the depths of the earth? Who will want

them? And now that I have shouted the message of the

world diamond industry so loudly and clearly, I’ll take

a deep breath and return to an orderly explanation.

There Was a Time

There was a time when a single — or almost single

— supplier dominated the world of diamonds,

determined the quantities supplied, the prices and the

fate of all parties in the market. This rough supplier —

and it is no secret that its name is De Beers — was

careful to check where the rough it sold went. Its

representatives would visit the clients periodically and

check whether each one was indeed using the rough for

the manufacturing purposes for which it was intended.

The world of diamonds was orderly and clear, governed

with a strict hand.

Although the past is always considered something

to yearn for, we remember clearly, and sometimes

painfully, that along with the great advantages of

having an all-powerful conglomerate, there were also

some major drawbacks. We benefited from its existence,

but we also complained. Among the drawbacks were

the constant differences between the monopolistic rough

market and the free polished market; the profit

immediately taken when we invented sophisticated

technology that improved our manufacturing

capabilities; the uncompromising requirement to take

rough in any quantity and at any price offered us, even

when times were very tough; and the need to constantly

come up with new creative ideas, sometimes “schemes,” in order to live with the demands of the supplier.

When new parties arrived on the rough scene —

first Australia with the direct marketing of Argyle

goods, then Canada and later direct supply from Russia

— and in light of the unsatisfactory share performance,

De Beers had to give up its past customs and adapt to the

new dynamics. Today, although it is considered a very

dominant and influential rough producer, one can no

longer attribute all the troubles of the market — nor all

its successes — to De Beers.

|

x |

| |

|

|

| |

a) Mr Moti Ganz, Honorary President of the International Diamond

Manufacturers Association and Chairman of the Israel Diamond Institute |

|

| |

The Emergence of Speculation

The deep change in the diamond industry took

place as the year 2000 approached. We flowed with the

changes, increased efficiency, updated, cut back,

expanded, made connections downstream and upstream

on the pipeline, developed brands, set up jewellery

companies, joined jewellery partnerships, split, merged,

adapted our companies to best business practices in the

diamond industry, set up manufacturing plants in

countries with low labour costs at one end of the world

map and in countries that promised rough supply at the

other end. We worked hard, we sweated, we thought,

we were creative — all in order to adapt to the new order

in the world diamond industry, and boost it as much as

we could.

We did excellent work. It seems to me that despite

some slumps and difficulties, we felt great confidence

in our industry. We knew we were moving forward.

In 2007-2008 the financial bubble in the world

began growing. The diamond industry did not remain

untouched, and became inflated as well, on the level of

finances as well as stocks. The price rises were crazy,

speculations as a result of the currency policies in South

Africa and India caused a loss of any connection between the market price of rough and the price of

polished. There were sightholders who used credit they

received not to manufacture but instead to invest in real

estate or the stock market. In 2008, long before the

global credit crisis, I already came out in the trade press

and in international forums against irresponsible

increases in rough prices, which were driven by

speculation. I warned that the unreasonable euphoria in

the world diamond industry was leading to unreasonable

demand for rough at unreasonable prices. At the World

Diamond Congress held in 2010 in Moscow, I stressed

the extremely serious risk of the unrestrained increases

of rough prices, and the danger lurking.

However, as long as there was money around, the

wheels continued to turn and everyone enjoyed the

party. Only a few, including myself, shouted out —

Beware! In this game of musical chairs somebody will

fall behind. Perhaps more than one. Perhaps everyone. |

|

| |

An Abrupt Halt

At the end of 2008 the world encountered the

global economic crisis, the roots of which could be

traced back to 2000, with the burst of the hi-tech

bubble, which caused a preference for investing in the

real estate market, in turn producing a new bubble of

irresponsible use of inexpensive money by means of

unfounded loans, which allowed unrestrained purchases

of apartments and houses.

When the crisis broke out, everything stopped in

place — activity in the financial market and activity in

the diamond industry. The rough producers understood

that they were the only ones who could regulate the

market, and reacted quickly. They reduced production

and/or closed mines for a given period, and allowed

their customers to leave goods on the table. The Russians

activated their shock absorber — the Gochran (the state

treasury), which purchased Alrosa’s production. |

|

|

|

|

| |

The global economic crisis exposed some of the

fundamental weaknesses in the diamond business,

particularly the accumulation of inventory and

erroneous pricing. The suddenness of the global crisis

highlighted the vulnerability of the diamond industry to

external economic fluctuations.

Most of the banks in most of the centres acted with

the utmost responsibility, supported by diamantaires

who streamlined their activities and brought money

from home. However, some banks chose to support the

diamond centres by providing unreasonably generous

credit lines — again the speculations flourished, again

the prices of rough increased and again we found

ourselves in a whirlwind.

I repeatedly called upon the diamantaires: Don’t

buy rough at any price they ask. But rough continued

being sold, the prices continued to rise and there was a

festival of speculation. The rough producers — all the

producers — benefited from their ringing cash registers.

In order to maximize their profits even further, the

rough producers embraced the tender method, in an

effort to draw maximum benefit from the sale. The

difference between the price of rough and that of

polished dwindled to near nothing, as did the

manufacturers’ profits.

The manufacturers, who buy rough in order to

process it, are disappearing — cutting back

manufacturing, closing factories temporarily or shutting

them down all together. Even the well-established

manufacturers have to close excellent, well-organized

factories. Some are still holding on by the skin of their

teeth. But how long can a manufacturer continue to buy

rough if it means absorbing losses? A month? Two

months? Three? Half a year? The situation is worrying.

I apologize that I can’t avoid quoting myself, but

I articulated this in the past so well that there really is no

need to reformulate it. I wish I could say these words are

no longer relevant, but regrettably that is not the case.

In 2010, I wrote: “In the mining world, annual reports

and speeches stress the term ‘sustainable development.’

This refers to activities that have commercial viability

in the long term. Somehow, too many producers seem

to believe that when it comes to selling their product,

the short-term optimization of revenues is more

important than the long-term sustainable development

of their clients’ businesses. However, just as there are

fewer long-term commitments for supply to

manufacturers, these manufacturers should realize every

morning, over and over again, that every time we buy

rough at irresponsibly high prices we are damaging our

own long-term prospects. At the end of the day, those

who overpay will disappear, and the rough supplier will

simply find someone else who may await the same fate.

It is easy to dismiss this with ‘it’s a free market.’ That

isn’t totally true. We are not playing on an even, level

field. Rough speculators may lose or win some money.

Manufacturers, however, have huge investments in

factories and infrastructure and a workforce to protect.” |

|

| |

|

|

| |

Recently the rough producers realized that if they

didn’t lower their prices there wouldn’t be anyone to

buy their goods. Reducing prices is a double-edged

sword — it is essential because the manufacturers can’t

pay the prices demanded anymore, but it is a blow for those who bought goods at high prices, and benefits

those who had the wisdom to leave those goods on the

table.

It’s Not the Crisis

Our industry is stagnating. Not just in our country,

but all over the world. We tend to blame the economic

crisis. There’s a recession in the United States, the

European economy is collapsing, we say. But even in

times of recession young people continue to get married.

There are still occasions to celebrate. Moreover, the

economic situation in the US is not bad at all. At any

rate, it is not bad enough to cause a total halt — at the

most, a slight decline. The reason lies in the diamond

industry itself. As soon as it was no longer possible to

use bank credit for speculation, and a market emerged

of high rough prices that couldn’t be transformed into

money, the rough buyers began to “choke” and realize

their rough at 10 to 15 percent below the price demanded

by the major suppliers. The manufacturers who had

signed long-term contracts had to continue buying

rough at high prices, and meet the rest of their needs by

purchasing rough at impossible prices through tenders.

I would like to remind you what I said about

tenders at the International Rough Conference held in

Israel in 2008. Addressing the rough producers, I said:

“You will surely ask why the manufacturer’s troubles

should concern you? From our point of view, you’ll

say, the situation is ideal. We produce rough, sell it at

tenders, fetch prices we never could have dreamed of,

and our profits leave no room for complaint.

“A tender or an auction can be an excellent

solution as a ‘window’ onto the market, or the sale of

special diamonds. However, they cannot be a standard

solution, because they harm the manufacturer.

“The rough diamond has no value on its own. The

rough producer can’t do anything with these diamonds.

There were attempts to turn diamond into a commodity.

To try and make diamonds behave like gold, copper,

iron or coffee. That attempt failed. The rough diamond

is not worth money like metals are. Rough diamonds

can’t be used like coffee beans can. The rough diamond

is worth money only after it is polished. The rough

diamond is valuable only to — the diamond

manufacturer. Only I, the manufacturer, know what I

am holding in my hand and what can be done with

rough.

|

|

| |

|

|

| |

“So that I, the manufacturer, will want the rough

that you produce, I need to receive it consistently, on

the basis of ongoing, regular sortings. That’s the only

way I can make commitments to chains and to stores.

That’s the only way I can commit to ‘programmes.’

That’s the only way I can promise you that the rough

you produce will be worth something to the customer in

the store, and not only in the internal trade between us.”

When I finished speaking there was applause.

That was very nice, but in practice — nothing changed.

I barked and the profits of the rough producers continued

to rise, at the expense of the manufacturers.

We can’t continue buying rough at a loss forever.

It is impossible to continue manufacturing under the

present conditions. Without manufacturing, there’s

nothing to sell. If there’s nothing to sell — it won’t be

long (perhaps the day has already come) before the

display window will fill with more jewellery set with

precious stones, pearls and synthetic diamonds. And if

the public gets used to buying them — who will be able

to turn the clock back? A closed door of a factory is a

door that has no chance of opening. The storeowners

are tired of hearing us whine and ask for higher prices

while manufacturers of synthetic diamonds give them

goods on memo — and with a significantly higher profit margin. At first they’ll show the synthetics in a corner

of the store, but within a few years, they’ll display them

throughout the store. Look what happened with pearls.

This is already happening. Many diamond

manufacturers are now starting to manufacture synthetic.

Many others are considering adapting their production

lines to synthetic. The manufacturing system exists.

The marketing system exists. Why use it to create losses

when you can use it to make a profit? The infrastructure

is there, and if the rough producers don’t quickly catch

the manufacturers by the tail and keep them close to a

profitable supply — they will be able to regret what

happened, but not change it. Only recently a wellestablished

American diamond manufacturer told me

that if he hadn’t opened a line for synthetic parallel to

his regular system, he wouldn’t have survived, and that

he’s considering adapting his entire manufacturing and

marketing system to synthetics. Rough producers — is

that the road you are hoping we will take?

|

|

| |

Last Call

Therefore, while until recently I addressed mainly

the diamond manufacturers, asking them not to buy

rough at unreasonable prices, I now turn mainly to the

rough producers. Dear producers: Rough diamonds are

meant to be polished for setting in jewellery. They can’t

be eaten. They can’t be planted. They can’t even be

used for speculative purposes any more. You can

speculate for a year, or two years, but at the end of the

day, the mouth of that volcano opens up and destroys

everything around it. The rough producers need to

understand that a business in which speculation plays a

major role is not a business. It is a bubble that has burst,

and if it develops again — it will burst again.

Rough producers and manufacturers are in the

same boat — everyone wants steady business. Rough

producers want to know that someone will buy the

rough they produce. Rough producers have a duty to

the countries in which the mines are located. They have

a duty to the governments and to the people. They have

goals they must meet. If they don’t have anyone to sell

the rough to, they will have to get out of the mining

business.

Therefore, the producers must find a way to

support and encourage manufacturers. And here I

repeat the lessons of the 1970s and 1980s. The rough

producers must give the manufacturers very strong

backing, enabling them to return to the sphere of work

and establish themselves firmly in the market by assuring

steady clients who can rely on regular, certain supply.

The rough producers must also cultivate the dealers, so

that they can appropriately help those who manufacture

in small and medium volume and their employees,

either by financing or by supplying smaller parcels in

attractive sortings.

My advice to rough producers is this: The return

of speculation is not the end of the manufacturers alone,

but of the entire diamond industry. |

|

| |

|

|

| |

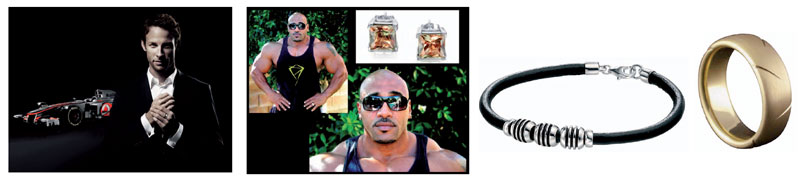

Men's Jewellery trends |

|

| |

In the basement of the famous

Hix restaurant in London’s Soho in

July, British jewellery brand Stephen

Webster invited guests to an early

morning fashion show for the

unveiling of its new jewellery collection. But this breakfast event

was not the usual showcase of

jewellery because, as the guests ran

their fingers over the new collection,

their attention was halted as, strutting

across the bar, appeared Spandau

Ballet brothers Gary and Martin

Kemp and famous hairdresser Nicky

Clarke, adorned with the brand’s

new collection — a range of men’s

jewellery — kitted out with the

sharpest tailored suits and smart,

lace-up shoes.

But what did this parade of

men’s jewellery mean? It represents

a shift in the direction of the men’s

market, a more grown-up movement

that puts the surf beads to one side

as jewellery of smarter origins and

even bespoke designs take centre

stage.

Mark Ungar, director of

Thorn.co.uk, the leading UK

website dedicated to branded men’s

jewellery, says that recent market

developments show that men are

looking for a bit of refinement in

their jewellery. Gone is the Russell

Brand look of chunky finger rings

and layered chains and rosaries,

and in is a classic, gentlemanly style

with delicate details and considered

design.

“We find it used to be theleather, surf bead jewellery that men

went for but now they want

something different,” Ungar

explains. “For example skulls —

we’ve been there, done that. Men’s

choices have calmed down a bit;

it’s about being smart now.”

Steffans in Northampton

boasts a strong online presence in

the UK with its collections of

branded jewellery that includes

men’s ranges from Links of London,

Thomas Sabo, Shaun Leane and

emerging brands such as ChloBoy,

the range from up-and-coming

fashion brand ChloBo. Steffans

founder and director Steff Suter says

that the men’s market has shifted

and that the grip of gothic men’s

jewellery is weakening.

|

|

| |

|

|

| |

The emerging trend, it

appears, is a desire for something a

little more sophisticated, a shift that

reflects the changes that have taken emerging trend for heavy tweed

jackets, rolled up ankle-length

chinos, polished leather shoes and

smart bags. Overall, men are more

confident experimenting with their

fashion while opting for premium,

well-made goods.

This appears to have filtered

down into jewellery design and, as

Ungar explains, consumers are

following fashion’s move towards

something a little more gentlemanly.

Single, understated rings, perhaps a

signet ring with a monogram or

cufflinks that do the talking are

becoming must-haves, even items

such as unusual tie pins are

becoming little objects of desire.

The signet ring is something

William Cheshire, founder of the

eponymous William Cheshire

brand, would love to see revived. “I

love a ring on the pinky finger, it

has a very ‘I’m in a private club

don’t you know’ look about it,” he

says. “[But] if there were any styles

I’d like to see the back of it would

have to be the Aussie leather

necklace, or a couple of beads,

Richard Hammond style – they’re

cool by the beach, but when the

City boys wear them it looks a bit

sad.” Essentially detail and interest appear to be taking hold in men’s

jewellery, a change that might be

the result of reining in design as the

industry and consumers continue to

work through the recession.

British jeweller Lewis

Williams, who works under the

brand name Lewis Henry Nicholas,

is a new designer on the scene and

though based in New York, says the

changes in demand for men’s

jewellery reflects a desire for quality

product with a story. He’s just been

snapped up by Kabiri, a fashionforward

independent jeweller in

London. “Recently men have

moved away from big hunks of

scary-looking jewellery and adopted

a more subtle approach,” he

explains. “I think men today are

genuinely interested in their

jewellery having a story and historic

references.” Williams adds that

taking design elements from

antiquity and interpreting them in

new ways is always going to be part

of men’s jewellery design. |

|

| |

|

|

| |

In Hatton Garden, fine

jeweller Nick Fitch, owner of

Nicholas James, has been making

bespoke jewellery for men for many

years. Last year he caused a stir

with a capsule high-end men’s

collection called Savage Solitaires

– solid gold rings with diamonds

and precious stones that referenced

the legend of Jack the Ripper.

Though Fitch’s work tends to be

mostly focused on fine men’s

jewellery such as wedding rings, he

too has noticed the move into

jewellery that represents a wider

shift in men’s fashion and shopping

habits. “The past two years leather

friendship bracelets became the

thing for guys, with little bits of

silver here and there – nothing

statement, quite casual,” explains

Fitch. “But suddenly I am seeing

guys, sharp dressed fellas in tailored

suits, and the last thing you expect

to see is a flash of gold bracelet

peeking out from under their cuff,

but that’s what they’re wearing

under their shirts.”

Stephen Webster meanwhile

says demand for his eponymous

men’s jewellery collection has

shifted. “In these difficult times

people tend to look for something a

little bit out of the ordinary and that

extra bit special – [the] reason why

our men’s jewellery sales are still strong,” he says.

Earlier this year Links of

London unveiled a steel jewellery

collection, made with the license of

British Formula One race team

McLaren. It was designed by

Philippe Cogoli, a former Alfred

Dunhill employee who has been

head of design of watches and

men’s jewellery and accessories at

Links of London for four years. He

says the market has grown and

revealed two types of male shopper.

“Men’s jewellery is not so niche

[now], its market has increased quite

a lot the last few years, definitely for

Links, our men’s market is growing

dramatically,” he explains. “Now

you have two types as such, those

guys who want something very

trendy and the guys who want

something more understated, with

that bit of something extra. They’re

the ones who are ready to spend

more money so want a bit more

value in the piece, a different shape

or some versatility.”

But how have men’s jewellery

brands adapted their collections to

fit with this market and with it the

pockets of the current male

consumer? Conventionally the

majority of men’s jewellery has

never quite been able to command

high prices, aside from bigger name

brands, wedding jewellery or fine

jewellery with gemstones, due in

part to the accessory connotation of

men’s jewellery. Further many male

shoppers were – and still are –

dipping their toes into the more

upmarket jewellery realm.

At Gecko Jewellery, where

men’s silver and steel collection

Fred Bennett is designed and

manufactured, price has always been

a key driver of each collection, to

maintain appeal for both retailers

taking on the products and the

eventual shopper. |

|

| |

|

|

| |

Hannah Trickett, head of

design at Fred Bennett, says the

gifting element to men’s jewellery

has meant designing with particular

price points in mind. “Price-wise,

steel jewellery has become a

bestseller over silver; because of its

ability to allow you to design

products that might become too

expensive if made in silver,” she

explains. “This has made steel very

appealing, but anything that goes

over the US$500 mark we struggle

to sell. That’s our top pricing limit.”

For Stephen Webster, a brand

known for its high-end jewellery

designs, the evolving price of the

raw materials has meant the brand

has had to adapt its collections;

something Webster says has been a

long-term, continuing challenge.

“We were never a brand who sold a lot of diamond men’s jewellery,”

he reveals. ”The price is always an

issue for wide appeal and also the

whole sparkly thing is too associated

with women’s jewellery and just

too pretentious for most guys.”

So does a more affordable

price go hand-in-hand with a simpler

design aesthetic? Possibly so, says

Ungar, who notes that the shift to

neat, more restricted styles of men’s

jewellery has come as consumers

tighten their belts. “Because of the

way the recession has affected

people I think the spend [on men’s

jewellery] is less compared to two

and half years ago,” he explains.

“When the going gets tough it’s the

classic with a little twist pieces that

sell.”

Cheshire agrees that male

customers often hunt around for a

good price, so he ensures that he

aligns his prices with those of his

retailers to retain fair competition.

“Mind you, it can be two years

before a customer comes back

[because] men tend to buy one thing

and really make it last,” he adds.

At Links of London the

McLaren range has been made

primarily in steel, with what it dubs

“masculine” materials such as

carbon fibre, Kevlar – the same

material used in bullet-proof jackets

– and black PVD used to give the

steel some personality.

Designer Cogoli says that

hitting key price points is always in

his conscious when designing, as

he has particular price targets to meet in his design briefs. “When

designing the current collection we

had several price points we had to

work to so I knew what I had to

achieve with the designs,” he

reveals. |

|

| |

|

|

| |

Nick Kovacs of IBB London,

owner and manufacturer of men’s

silver cufflinks and jewellery brand

Hoxton London, says that its

customer’s tastes have got a little

more adventurous but that

customers are still looking for classic

designs with small points of interest.

“Spinning rings, hinged bangles and

patterned cufflinks are becoming

bestsellers,” Kovacs explains.

“We’ve found the men’s market is

showing continual growth at a time

when very few product areas are

doing so.”

For Fitch, the majority of his

men’s jewellery sales will be of a

higher price due simply to the nature

of his work. However he

understands how the price of a piece

of jewellery really can make or break

a purchase. “Most men will spend

$50 or so on a friendship bracelet

[but] others will save thousands for

something special. Right now

they’re a minority, but a growing

one.” Fitch explains that men’s

jewellery is now beyond the fad

stage and that as the men’s watch and accessories market booms with

more men opting for higher-priced,

automatic watches or fine leather

goods, the men’s jewellery market

is beginning to follow.

While the high street has

enabled fashion retailers to

introduce men’s jewellery

collections, some designers have

found this has made attitudes

towards men’s jewellery difficult to

alter. Cheshire explains that it is

sometimes difficult to get male

customers through the door of a

jewellery shop purely because it is

retail space they will be largely

unfamiliar with. “[Male shoppers]

are more inclined to see jewellery in

fashion stores, such as All Saints or

Topman for example,” says

Cheshire. “This is usually quick

fashion items aimed at the youngermarket [but] the independents are

getting in on the game, allowing

more space in the stores and using

the web to portray a more masculine

image.”

The online arena appears to be the most important platform for

driving men’s jewellery sales,

however, as it allows them to sit

back and browse products, compare

prices and make purchases without

having to enter a store — perhaps

an ideal, comfortable middle ground

for shoppers who might not yet be

prepared to step over the threshold

of a store to try on a necklace or

ring. |

|

| |

|

|

| |

Ungar’s customer base

certainly supports this view. He has

found that his international

customers appear a lot more comfortable shopping online, and

while UK sales are steady most UK

shoppers will make entry-level trial

purchases before shopping for more

expensive goods. “We sell a lot

online to America and Australia

and have had a number of shoppers from Russia,” he explains. “The

Americans are more than happy to

shop online and so they will spend

more, while the UK’s men’s market

is more about trying out shopping

online with a small purchase of

around $250.”

Cheshire concurs: “I found

the majority of my website orders

are from men, so I’m inclined to

suggest chaps prefer to shop around

online rather than go for the impulse

buy from a shop.”

At Thorn, marketing has been

key and the use of search engine

optimisation, Google Ad Words and

pay per click initiatives ensures that

the company remains top of search

results through Google. “We make the most use of key words that are very simple search terms, plus particular designer names that we know will be popular searches as well," explains Ungar.

Even online retail giants such as Asos are host to men's jewellery, not only own-branded products but also fashion-led collections from Simon Carter, Vivienne Westwood and Armani. Of note, however, is the lack of men's precious or silver jewellery, perhaps due to its target market. Conversely, high-end men's fashion site Mr. Porter, brother site to luxury women's retailer Net-a-Porter, does boast a capsule collection of men's jewellery including 18K gold and bllodstone signet rings.

|

|

| |

|

|

| |

As with any industry as time evolves new faces come through and, along with Lewis William's collection of jewellery, several other designers have been tipped for the top by the industry. Both Stephen Webster and William Cheshire namecheck Tomasz Donocik as their rising star of men's jewellery and thought he is not the newest player on the scene, his designs have certainly caused a stir, with Webster describing him as "a very dynamic guy" and Cheshire admiring his "good feel for men's jewellery, style and wearability"

Thorn's Mark Ungar meanwhile is supporting emerging designer Lukasz Pasikowski, founder of Cardinal of London. Ungar spotted his work at Treasure at Jewellery Week in June and commends him for offering something a little different with his selection of hand-crafted animal head men's jewellery and bangles and rings that appear hewn from rocks.

Nick Fitch has also reacted to the changing market and, designed to launch simultaneously with a new Nicholas James website his month, he will reveal a new carefully priced men's jewellery collection designed in partnership with his long-term collaborative partner Harcourt, a leather specialist. The new range will be priced upwards of $325 and will include items that can be traditionally monogrammed or set with birthstones.

Certainly it appears that the men's jewellery market has moved on, or at least in a newdirection as men begin to appreciate design and want more from their jewels. While there are still plenty of entry-level options such as the ranges from Fred Bennett and Hoxton London, the rise in men looking fo items unique to them that have a classic, gentlemanly aesthetic shows a return to safe, quality goods that will might command a premium price but will ultimately last.

|

|

| |

|

|

| |

The Transition from Diamond Dealers to Jewellery Manufacturers

By: Iris Hortman, Israel Diamond Institute Information Officer

|

|

| |

Over the years, the Israeli

Diamond Industry has focused on

selling an assortment of diamonds

— both rough and polished

diamonds. In the opinion of most

diamond dealers, the design,

production, import and export of

jewellery were not considered to be

an effective way of promoting or

marketing the diamonds in their

possession. But times have changed:

the Israeli diamond industry has

undergone changes and the

worldwide jewellery industry has

experienced globalization. The

attitude that a piece of jewellery can

promote diamond sales has been

changing in recent years.

The marketing of diamonds

embedded in jewellery produces an

added benefit for the exporter,

because the sale of a piece of

jewellery embedded with diamonds

maximizes the profit from the

diamonds, which can reach 20%. In

addition, embedding diamonds in

jewellery allows for the use of

diamonds of lesser clarity, which

constitute the bulk of the diamond market. Embedding a diamond in a

piece of jewellery can, if done

correctly, hide the diamond’s

imperfections with its metallic

components.

Today it is much easier for

diamond dealers, even those

working at a smaller scale, to market

diamonds embedded in pieces of

jewellery. It is easy to acquire pieces

of gold jewellery ready for

embedding, and embed within them

any diamond, and then to sell it

already embedded within the piece

of jewellery. A diamond dealer is

not required to maintain a collection

or inventory of pieces of jewellery

-- he or she can respond individually

and immediately to the customer’s

preferences regarding a piece of

jewellery, by acquiring a piece of

jewellery ready for embedding. |

|

| |

|

|

| |

In spite of that, if diamond

dealers insist on developing unique

models, they can be ordered from

specialty stores, or one can learn

how make them oneself, with the

aid of computer programmes

available on the market. The

jewellery production process has

been greatly simplified these days,

using computerized design

programmes, which allow one to

examine the piece of jewellery from

every possible angle, to calculate in

advance the amount of material

needed, and even its sale price. The

computer sends a file with all the

required information to a special

printer which smelts the models

directly into moulds ready for the

next stage of the production process

— the creation of rubber moulds,

and the production itself.

In recent years, a labour force

highly skilled in all tasks related to

jewellery production has joined the

Israeli industry: the wave of

immigration to Israel from the

former Soviet Union. These

migrants brought with them

reservoirs of knowledge, skills and

abilities that advanced the jewellery production and embedding

industry.

With all of these advantages,

why wouldn’t diamond dealers use

the embedding of diamonds in

pieces of jewellery as a way to

leverage their marketing of

diamonds?

Some diamond dealers

believe that the changes in

accounting and processing that

would be required in the transition

from the export of diamonds to the

export of jewellery will pose

challenges. |

|

| |

The export of jewellery does

not require one to pay Value Added

Tax, but it requires that it be

reported, something that is not the

case with the export of diamonds.

Diamond dealers are hesitant to

adopt this step because it would

require changes in their accounting

systems, the establishment of an

additional company or legal body

and extra expenses. Though it

should be recalled that VAT may

add to the workload, and also

perhaps be an additional expense

to the diamond dealer, it does not

require a capital expenditure. As

well, diamond dealers who open a

VAT account can receive VAT

refunds on moneys spent on

materials and labour to create and

embed the jewels.

Another process that

exporters must adjust to in the realm of jewellery essentially results

from the need to record the export,

like all products exported from

Israel. The record is carried out by

a customs official via an agent,

which necessitates a fee, as opposed

to the way it is done currently, at the

customs desk in the Israeli Diamond

Exchange. |

|

|

The jewellery delivery

process, as opposed to diamond

exports which are carried out

directly from the exchange itself,

are carried out via delivery

companies, using couriers or secure

couriers. This process can

sometimes involve an extra fee in

addition to the cost of delivery,

such as a charge for storing the

merchandise in a safe. This storage

fee can sometimes be quite high in

the event that the delivery does not

take place over business days, but

on weekends or holidays. This

problem can be overcome by

advance planning of the export

process.

Certainly, there are ways to

reduce the expenses associated with

jewellery exports. In conversations

I have had with diamond dealers

and jewellery manufacturers for the

purposes of this article, several

methods of making the export

process easier were suggested. For

example: opening an additional

customs office at the diamond

exchange for the benefit of diamond

dealers who require jewellery export

services, in order to make it easier

to possess pieces of jewellery for

the purpose of repairing them, and

other similar uses.

The export of jewellery

produced in Israel entails the

advantage of the priority status they

are granted by customs. Israeli-made

jewellery falls under the free-trade

agreements which Israel has with

other countries, such as the United

States and Europe, and is therefore

exempt from customs fees. This

advantage will only increase as

Israel’s trade agreements are

expanded upon, especially with the

countries of East Asia.

The sale of jewellery

embedded with diamonds advances

the diamond trade. In this way,

diamond dealers can work directly

with the final customer, the jewellers,

in order to save themselves

middleman fees and thus maximize

their profits.

|

|

|

| |

|

|

|